Payroll Tax is a state tax collected on wages once the applicable threshold has been met.

The current threshold for Queensland is $1,100,000.

If you employ people in other states then you would need to be aware of that states threshold.

In order to assess whether you need to register for payroll tax and have reached the threshold you need to calculate your taxable wages. The following are included in this calculation -:

- allowances

- bonuses

- commissions

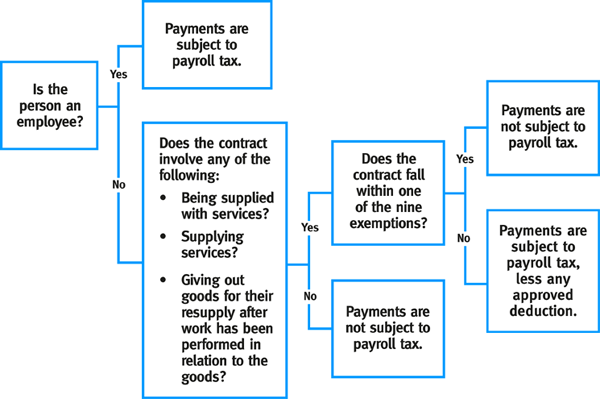

- contractor payments - Any payments you make to contractors, subcontractors and consultants are taxable unless they meet one of the 9 contractor exemptions. If you are required to pay payroll tax on payments to a contractor who provided materials and equipment, you may be eligible to apply an approved non-labour deduction.

- fringe benefits - calculated on the Type 1 and Type 2 aggregate amounts grossed up by the Type 2 gross-up factor. Fringe benefits that have a nil taxable value under the Fringe Benefits Tax Assessment Act 1986 will also have a nil taxable value for payroll tax purposes

- directors remuneration - This may include payments to a director's trust or incorporated entity

- salary

- superannuation contributions –including payments to non-employee directors. Include any superannuation payments paid outside your payroll system (e.g. top-up payments to a director's superannuation fund).

- wages (cash and non-cash).

There are some exemptions, mainly payments to apprentices employed under the Further Education and Training Act 2014 (FET Act) are generally exempt.

Payments to trainees registered under the FET Act are exempt unless before commencing the traineeship, the trainees worked for you for either:

- 3 months or more full time

- 12 months or more, part time or casually

Payroll Tax on Contractor Payments is a main focus at present by the Office of State Revenue, the rules governing this component of the Act are under Division 1A.

An independent contractor is an entity that agrees to produce a specific result for an agreed price. Contractors can include:

- sub-contractors

- consultants

- sole traders

- companies

- partnerships

- trusts.

In most cases a contractor:

- is paid for results achieved

- provides all or most of the necessary materials and equipment to complete the work

- is free to delegate work to other entities

- has freedom in the way the work is done

- provides services to the general public and other businesses

- is free to accept or refuse work

- is in a position to make a profit or loss.

You only need to satisfy one of the following nine exemptions for your contractor payment to be exempt from payroll tax.

- Services are provided for no more than 90 days in a financial year, these days do not need to be consecutive.

- Services required by your business for less than 180 days in a financial year (Read the public ruling on the contractors 180-day exemption (PTA020) for more information.

- Services performed by 2 or more people, where the contractor engages others to provide the services they are contracted for, or 2 or more people are needed to fulfil the contract.

- Services ancillary to the supply of goods, as in a crane operator for a crane that is hired.

- Services not ordinarily required by your business, an example being a bank that hires a painter to paint its office.

- Services approved by the Commissioner as exempt, this needs to be applied for on a case by case basis.

- Services provided by an owner-driver, if the main purpose of the contract is to deliver goods.

- Services relating to door-to-door sales, if you contract to sell goods door to door for domestic purposes.

- Services relating to selling insurance, if genuine contractors with an agency business

Payroll tax can be a very complex matter and a costly one to get wrong. Please contact your Ulton advisor should you need assistance with any business tax issue.

Click here to read more about 'Grouping' Payroll Tax in Queensland