A feature of this Budget is its focus on economic recovery by encouraging Australians to spend money and incentivising job creation.

From a taxation perspective this is principally achieved by the following tax measures:

- Bringing forward the personal tax cuts and backdate their introduction to 1 July 2020

- Providing business with an outright tax deduction for expenditure on the acquisition of assets; and

- Introducing loss carry back rules which allow a corporate entity to offset losses in the next two years against the profits (and tax paid) for the 2019 & 2020 years.

There are other tax measures which will assist business and individuals:

Business

- Extension of the definition of a small business entity to include an entity which has a turnover of up to $50m. In conjunction with this change, the SBE concessions are extended to a wider taxpayer group;

- Changes to FBT applicable to various benefits provided to employees – car parking, electronic devices;

- Modification to the R & D rules by altering the unnecessary changes to the concessions introduced by Treasury Amendment (Research & Development Tax Incentive) Bill 2019; and

- Clarification of the residency rules applicable to foreign incorporated companies.

Individuals

- CGT will not apply to the creation, variation or termination of a granny flat arrangement providing accommodation where there is a formal written agreement in place.

The exemption will only apply to agreements that are entered into because of "family relationships or other personal ties" and will not apply to commercial rental arrangements.

Details of the principal measures

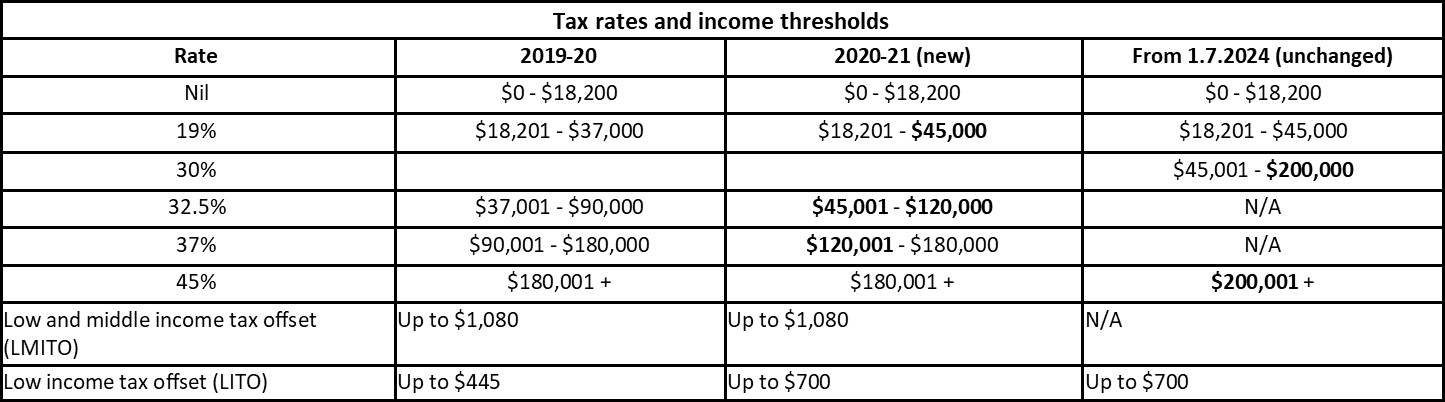

Personal Tax Cuts

In summary from 1 July 2020:

- the low income tax offset will increase from $445 to $700;

- the top threshold of the 19 per cent tax bracket will increase from $37,000 to $45,000; and

- the top threshold of the 32.5 per cent tax bracket will increase from $90,000 to $120,000.

Rates and threshold tables

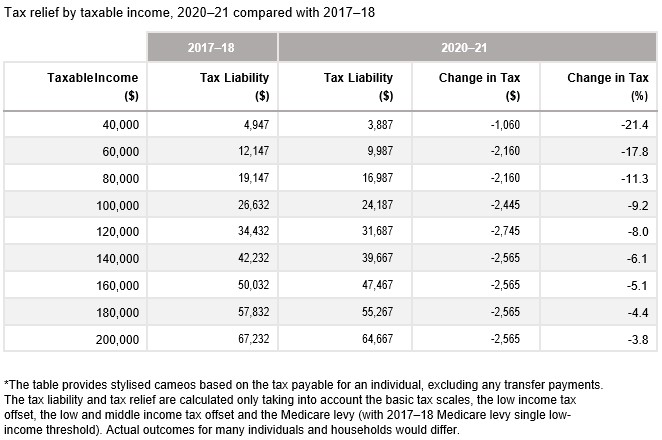

The actual cash impact of the above rate changes are illustrated by this table provided in the budget papers:

Asset write off rules

The proposed rules provide:

- Businesses with annual aggregated turnover of less than $5 billion will be entitled to an immediate tax deduction for the full cost of new eligible capital assets and improvements to existing eligible assets acquired from 7:30pm AEDT on 6 October 2020 and first used or installed by 30 June 2022.

- Businesses with aggregated turnover of less than $50 million will also be entitled to an immediate tax deduction for the full cost of second-hand assets acquired from 7:30pm AEDT on 6 October 2020 and first used or installed by 30 June 2022.

- Businesses with aggregated annual turnover between $50 million and $500 million can claim an immediate deduction for the full cost of eligible second-hand assets costing less than $150,000 if they are purchased by 31 December 2020 and installed ready for use by 30 June 2021

- Small businesses with aggregated turnover of less than $10 million can deduct the balance of their simplified depreciation pool at the end of the income year.

Loss carry back rules

The proposed measures will provide temporary tax relief by allowing eligible corporate entities (that is, entities with a aggregated turnover of less than $5 bn) to elect to carry-back tax revenue losses made in the years ending 30 June 2020 to 2022 to offset tax paid on profits made during the 2019 income year onwards.

There are importantly some limitations in relation to this measure:

• Losses carried back cannot exceed earlier taxed profits;

• The carry-back amount must not generate a franking account deficit; and

• It does not apply to other types of entities – trust, partnership or sole trader.

For corporate entities that elect to apply this measure, they will receive a tax refund in the loss-making year equal to the tax which has been offset by the losses carried back.

The franking account deficit limitation will be a significant impediment to the practical implementation of the measure. It is not unusual for small companies to pay franked dividends to its shareholders during profitable years, first as a return to the shareholders but also to offset Division 7A loan arrangements. In both instances the franking credits generated by tax paid are offset by the franking credits applicable to the franked distributions.

Note that if the corporate entity does elect to use the loss carry back rules, the loss will be able to be carried forward in accordance with the existing loss rules (Division 165 & Division 166 ITAA 1997).

We're here to help

If you have any questions or concerns about the proposals from the Federal budget announcements, please contact your Ulton Advisor to discuss.

Learn more

Want to read We have broken the full budget down into 6 main categories for usability.